After 37 years of clocking in and out of work and religiously saving at least 10% annually in my 401K every year, my countdown to financial independence is in sight. Each month is a step closer and let’s look at how this past month is getting me there.

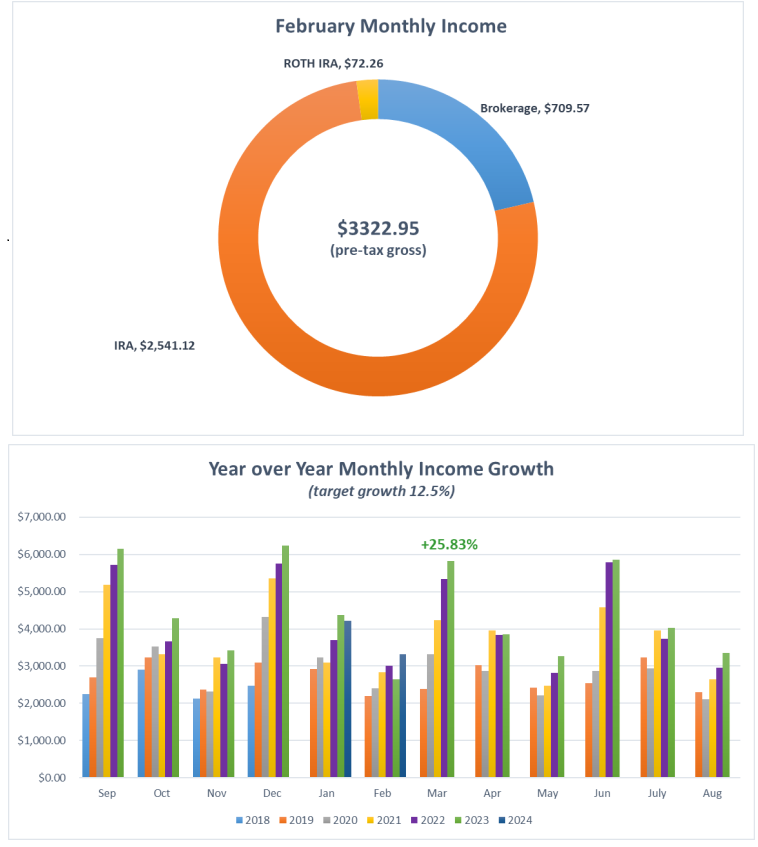

For the month of April I made $4,407.44; an increase of 14.42% versus this time last year. Not too shabby and well above my 12.5% target.

Regarding raises, I received 6 dividend raises from BHB, IBM, JNJ, PG, PSX & SO that added $121.97 to my forward annual income.

In regards to my portfolio positions, my M1 finance accounts were fully transferred to Fidelity and I can finally close that chapter. I still have some cleanup work to do but overall happy it went as smoothly as possible. On the investing front I will no longer be adding any funds to my brokerage account and all investing will be limited to my Roth IRA and 401K. Starting in May any surplus cash will be saved in a money market to build a cash pile for retirement which is rapidly approaching.

Last month in my “On the Home Front” section I told you my company was going to have significant layoffs on May 1. When the big day came I was passed over. I volunteered for the layoff to save someone else’s job but what I did not know was 3 other people in my group did the same. My manager had enough volunteers to meet a quota and choose to keep me on. I cannot speak for the rest of my company but for my group everyone that needed a job got to stay and that is what matters.

Enough of me babbling, here are the numbers:

Dividends Received

| Date | Symbol | Company | Amount |

| 4/1/24 | AGR | AVANGRID | $26.05 |

| 4/1/24 | ARCC | ARES CAPITAL CORP | $588.39 |

| 4/1/24 | AVGO | BROADCOM INC | $10.97 |

| 4/1/24 | DIVO | AMPLIFY ETF TR CWP ENHANCED DIV | $129.29 |

| 4/1/24 | GRMN | GARMIN LTD | $80.69 |

| 4/1/24 | IDVO | Amplify International Enhanced Dividend Income ETF | $85.31 |

| 4/1/24 | KHC | KRAFT HEINZ CO | $10.47 |

| 4/1/24 | LMT | LOCKHEED MARTIN CORP | $29.59 |

| 4/1/24 | PEP | PEPSICO INC | $68.58 |

| 4/2/24 | BEPC | BROOKFIELD RENEWABLE CORP | $81.43 |

| 4/2/24 | KMB | KIMBERLY-CLARK CORP | $18.77 |

| 4/4/24 | IRM | IRON MTN INC | $525.53 |

| 4/4/24 | TU | TELUS CORPORATION | $68.19 |

| 4/5/24 | MRK | MERCK &CO. INC | $171.18 |

| 4/11/24 | BBY | BEST BUY CO INC | $24.56 |

| 4/15/24 | EPR | EPR PROPERTIES | $88.59 |

| 4/15/24 | NEWT | NEWTEKONE INC | $206.55 |

| 4/15/24 | O | REALTY INCOME CORP | $87.80 |

| 4/15/24 | PKG | PACKAGING CORP OF AMERICA | $24.67 |

| 4/15/24 | WPC | WP CAREY INC COM | $486.59 |

| 4/16/24 | ACRE | ARES COMMERCIAL REAL ESTATE CORP | $206.93 |

| 4/17/24 | BCE | BCE INC | $462.33 |

| 4/17/24 | CPT | CAMDEN PROPERTY TRUST | $15.80 |

| 4/18/24 | PSEC | PROSPECT CAP CORP | $98.13 |

| 4/23/24 | MAIN | MAIN STR CAP CORP | $45.14 |

| 4/26/24 | OGE | OGE ENERGY CORP | $164.14 |

| 4/29/24 | AMNF | ARMANINO FOODS DISTINCTION INC | $200.36 |

| 4/29/24 | NUSI | ETF SER SOLUTIONS NATIONWIDE NASDQ | $20.92 |

| 4/30/24 | BNS | BANK OF NOVA SCOTIA | $42.62 |

| 4/30/24 | UTG | REAVES UTILITY INCOME FUND | $239.99 |

| 4/30/24 | XRMI | GLOBAL X FDS S&P 500 RISK | $28.44 |

| 4/30/24 | XYLD | GLOBAL X FDS S&P 500 COVERED | $69.44 |

Dividend Changes

| SYM | 2024 | 2023 | Difference | % Change | Notes |

| ACRE | $206.93 | $252.35 | -$45.42 | -18.00% | dividend cut |

| AGR | $26.05 | $24.81 | $1.24 | 5.00% | |

| ALL | $0.00 | $5.46 | -$5.46 | -100.00% | Sold Position |

| AMNF | $200.36 | $0.00 | $200.36 | 100.00% | Includes special div |

| AQN | $0.00 | $206.66 | -$206.66 | -100.00% | Sold Position |

| ARCC | $588.39 | $588.39 | 100.00% | 2023 Payout in Mar | |

| AVGO | $10.97 | $10.97 | 100.00% | 2023 Payout in Mar | |

| BBY | $24.56 | $22.90 | $1.66 | 7.25% | |

| BCE | $462.33 | $430.45 | $31.88 | 7.41% | |

| BEPC | $81.43 | $73.91 | $7.52 | 10.17% | |

| BNS | $42.62 | $38.94 | $3.68 | 9.45% | |

| CPT | $15.80 | $15.34 | $0.46 | 3.00% | |

| DIVO | $129.29 | $110.98 | $18.31 | 16.50% | |

| EPR | $88.59 | $85.49 | $3.10 | 3.63% | |

| GRMN | $80.69 | $79.55 | $1.14 | 1.43% | |

| GSK | $0.00 | $94.02 | -$94.02 | -100.00% | Sold Position |

| IDVO | $85.31 | $85.31 | 100.00% | New Position | |

| IRM | $525.53 | $500.07 | $25.46 | 5.09% | |

| KHC | $10.47 | $10.47 | 100.00% | 2023 Payout in Mar | |

| KMB | $18.77 | $18.00 | $0.77 | 4.28% | |

| LEG | $0.00 | $311.45 | -$311.45 | -100.00% | Sold Position |

| LMT | $29.59 | $29.59 | 100.00% | 2023 Payout in Mar | |

| MAIN | $45.14 | $38.57 | $6.57 | 17.03% | |

| MPW | $0.00 | $222.94 | -$222.94 | -100.00% | Sold Position |

| MRK | $171.18 | $162.29 | $8.89 | 5.48% | |

| NEWT | $206.55 | $148.85 | $57.70 | 38.76% | |

| NUSI | $20.92 | $0.00 | $20.92 | 100.00% | 2023 Payout in May |

| O | $87.80 | $11.32 | $76.48 | 675.62% | |

| OGE | $164.14 | $150.31 | $13.83 | 9.20% | |

| PEP | $68.58 | $68.58 | 100.00% | 2023 Payout in Mar | |

| PKG | $24.67 | $23.86 | $0.81 | 3.39% | |

| PSEC | $98.13 | $98.13 | $0.00 | 0.00% | |

| TU | $68.19 | $60.70 | $7.49 | 12.34% | |

| UTG | $239.99 | $239.99 | 100.00% | New Position | |

| WMT | $0.00 | $15.01 | -$15.01 | -100.00% | Sold Position |

| WPC | $486.59 | $589.85 | -$103.26 | -17.51% | dividend cut |

| XRMI | $28.44 | $0.00 | $28.44 | 100.00% | 2023 payout in May |

| XYLD | $69.44 | $0.00 | $69.44 | 100.00% | 2023 payout in May |

| M1 Finance | $0.00 | $59.75 | -$59.75 | -100.00% | account closed |

| Total | $4,407.44 | $3,851.96 | $555.48 | 14.42% |